October 2019

By: Pat Guinet, CIMA®

“Yield curve inversion” has been in the news lately. You may be wondering exactly what this is, what it portends, and why it’s getting so much press. There are rare times when long-maturity bonds have a lower interest rate than short-term interest rates.

What does this mean for us as investors?

In simplified terms, when short-term rates are higher than long-term rates, the market is saying: “Good times are here … but bad times are coming.” Central banks typically raise interest rates to curb inflation as the economy strengthens but lower interest rates to stimulate business activity when the economy is struggling.

Consider the following: As we write this (9/30/19), a 10-year Treasury note is yielding about 1.68%. Meanwhile, a 3-month Treasury bill (T-Bill) is yielding 1.88%. Assuming investors have a long-term time horizon, what would make them buy the lower-yielding, more volatile long-term bond, rather than just rolling over a series of three-month investments in higher-yielding, less volatile T-Bills?

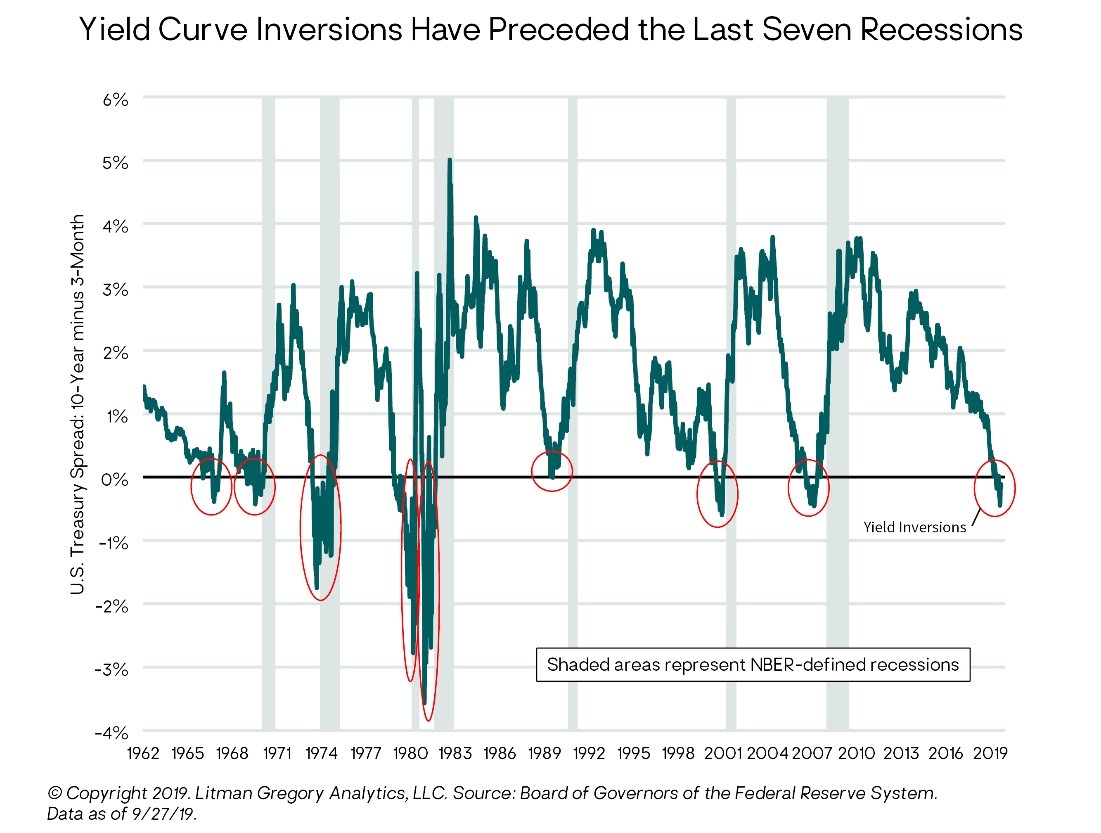

Choosing the 10-year note makes sense if an investor thinks interest rates will fall enough over the next 10 years that locking in a 1.68% long-term return would produce at least as good a result as a series of short-term bonds. Typically, some kind of recessionary event would be necessary to cause short-term rates to decline. Indeed, an inverted yield curve has preceded the last seven U.S. recessions. This is why many investors are concerned.

It’s important to remember, however, that the yield curve reflects investors’ expectations for interest rates, inflation, and economic growth. Investors are human after all; there’s no guarantee that the market’s collective prediction will come to pass. A recession did not follow the yield curve inversion in 1966.

Why it could be different this time?

Many commentators have offered up plausible reasons why a yield curve inversion may not be indicating an imminent recession today:

All these factors could be involved in keeping long-term yields low, while short-term rates remain higher after the Federal Reserve’s recent program of rate hikes.

What is Guardian Financial Partners doing?

No single indicator, however reliable in the past, is sufficient to make an investment decision. We recently upgraded the quality of fixed-income holdings in client portfolios, but we did so upon consideration of several data points that were signaling concerns. Fixed-income holdings should now respond better if the current yield curve inversion and other signs we see are correctly identifying a coming recession. The role of fixed-income is first and foremost to provide support to portfolios during deflationary events and bear markets in stocks.

We are always likely to hold some allocation to global stocks, and as investors, we must accept that this allocation is where the largest potential return and risk lies. The opportunity cost of making dramatic adjustments with binary outcomes on the equity side of portfolios (such as selling out of stocks completely due to a recession prediction) is too great if you turn out to be wrong. There could very well be a cyclical rebound that extends this cycle, in which case we’d expect international and value stocks to perform well given their greater sensitivity to global growth. Our holdings in those areas balance the increased defensiveness we have in place on the fixed-income side. Your portfolio should thus be resilient in either scenario—recession or cyclical rebound. If you have questions or would like to review your financial situation, please click here to view our calendar.

Certain material in this work is proprietary to and copyrighted by Litman Gregory Analytics and is used by Guardian Financial Partners with permission. Reproduction or distribution of this material is prohibited and all rights are reserved.